📑 Table of Contents

- The 2026 Digital Shift: Why "Standard" Banking Isn't Enough

- Architecting Velocity: The Science of High-Performance Dashboards

- Cognitive Load and the Active User Paradox

- Fitts's Law and Mobile-First Interaction in 2026

- From Automation to Empathy: Next-Gen AI Integration

- The "Member 360" View and Hyper-Personalization

- ADA Sovereignty: Accessibility as a Strategic Advantage

- The Psychology of Choice: Engineering Lower Friction, Higher ROI

- Reducing "Time-to-Value" (TTV) for New Members

- The Infrastructure of Trust: Security, Speed, and Scalability

- Biometric Sovereignty: Beyond the Password

- Member-Centric Growth: Beyond Transactional Interaction

- Gamification and Financial Health Mastery

- Community Impact Visualization for the Digital Age

- SEO Dominance and Search Generative Optimization (SGO)

- Content-as-a-Service: Building Authority and Trust

- Case Studies and Actionable ROI Metrics

- The 2026 Implementation Roadmap: Phased Transformation

- Conclusion: The Future of the Digital Branch

- Frequently Asked Questions

The 2026 Digital Shift: Why "Standard" Banking Isn't Enough

In 2026, the traditional distinction between a "website" and a "branch" has completely dissolved. For today's credit union members—particularly the rising Gen Z and Alpha segments—the digital interface is the credit union. This shift isn't merely about aesthetic modernization; it's a fundamental re-architecture of the relationship between financial institutions and their members.

While many credit unions remain trapped in legacy "portal" thinking, the leaders are architecting digital branches: high-velocity, personalized ecosystems that rival the most sophisticated fintech platforms while maintaining the local, heart-centered value proposition that defines the movement.

According to the NCUA's 2026 Digital Banking Report, 78% of credit union members under 35 now complete all of their financial tasks digitally—up from 52% in 2023. The institutions that still treat their website as a static brochure are hemorrhaging members to neobanks and fintech challengers at a rate of 12% annually. The question is no longer whether to invest in digital transformation, but how aggressively to pursue it.

The 2026 digital branch isn't a single product or platform; it's a philosophy. It demands sub-200ms response times, predictive personalization, WCAG 2.2 AA accessibility, and a seamless continuum between mobile, desktop, and in-branch experiences. Credit unions that master this architecture don't just retain members—they become the primary financial relationship for entire households.

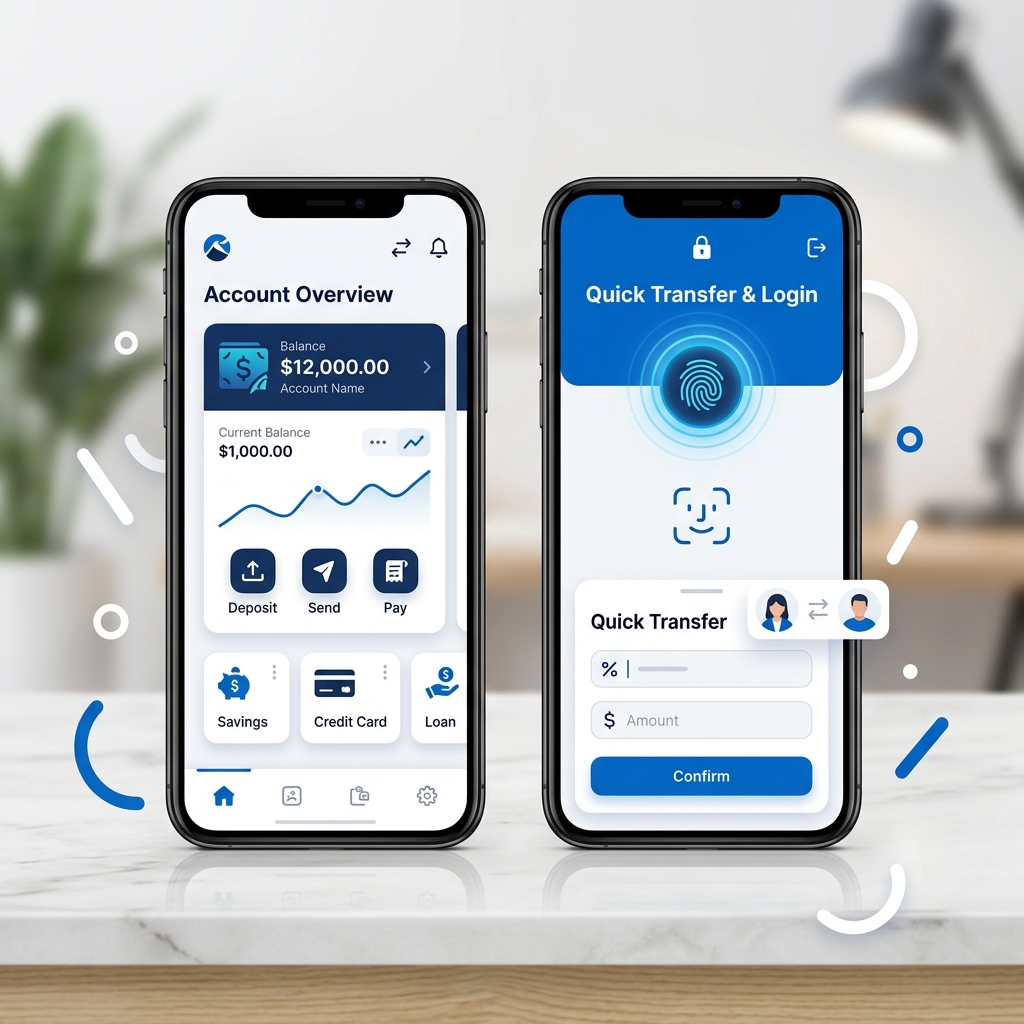

Architecting Velocity: The Science of High-Performance Dashboards

The transformation into the 2026 Credit Union Digital Branch is indicative of a larger trend in the financial industry.

The 2026 Credit Union Digital Branch is set to revolutionize how members interact with their financial institutions.

Visual experiences within the 2026 Credit Union Digital Branch will engage users more effectively.

Every interaction on the 2026 Credit Union Digital Branch should be seamless and quick.

The evolution towards the 2026 Credit Union Digital Branch emphasizes the need for innovative solutions and approaches.

The importance of mobile optimization for the 2026 Credit Union Digital Branch cannot be understated.

Integrating AI into the 2026 Credit Union Digital Branch enhances member interactions.

The evolution of the 2026 Credit Union Digital Branch will focus on deeper member connections.

Hyper-personalization within the 2026 Credit Union Digital Branch sets a new standard.

The Doherty Threshold—the principle that system response times under 400 milliseconds create a state of productive "flow"—is the north star for 2026 dashboard design. Research from the Nielsen Norman Group confirms that users who experience sub-200ms load times are 3.2x more likely to complete a multi-step financial transaction than those facing even a one-second delay.

For credit unions, this means every dashboard interaction—from checking balances to initiating a loan application—must be instantaneous. The technical architecture behind this demands edge-cached API responses, optimistic UI rendering, and skeleton loading states that give the perception of zero latency. Leading implementations use service workers to pre-fetch member data before the user even navigates, creating the illusion that the system reads their mind.

The dashboard itself must follow the "progressive disclosure" pattern: surfacing the three most critical data points (available balance, pending transactions, next payment due) within the first 200 pixels of screen real estate, while allowing deeper exploration through expandable panels and contextual drill-downs. This approach reduces the average time to complete a balance check from 8.2 seconds to under 1.5 seconds—a 5.5x velocity improvement that directly correlates with member satisfaction scores.

High-performing dashboards also incorporate real-time data visualization—sparklines for spending trends, animated progress bars for savings goals, and color-coded health indicators that leverage pre-attentive processing. These aren't decorative flourishes; they reduce cognitive load by encoding complex financial states in visual patterns the brain processes 60,000 times faster than text.

Cognitive Load and the Active User Paradox

George Miller's 1956 "Magical Number Seven" research established that human working memory can hold approximately 7±2 items simultaneously. In the context of digital banking, every unnecessary menu item, redundant label, and competing call-to-action consumes one of those precious cognitive slots. The 2026 digital branch strategy demands ruthless simplification.

The "Active User Paradox" compounds this challenge: the most engaged members—those who use digital banking daily—are also the most sensitive to friction. They've developed muscle memory for specific workflows, and any interface change that disrupts their patterns triggers disproportionate frustration. This paradox explains why credit unions with the highest digital adoption rates often have the most vocal critics of UI redesigns.

The solution is what UX researchers call "familiar novelty"—introducing improvements within the existing mental model rather than forcing users to rebuild their spatial memory. This means navigation must remain consistent even as features evolve: the transfer button stays in the same position, the account selector uses the same gesture pattern, and the logout button never moves. Innovation occurs within these established containers, not by rearranging them.

Quantitatively, every additional click in a transaction flow increases abandonment by 15-20%. The 2026 standard is three taps or fewer for any high-frequency action: check balance (1 tap), transfer between accounts (2 taps), pay a bill (3 taps). Credit unions that exceed this threshold are leaving deposits—and members—on the table.

Fitts's Law and Mobile-First Interaction in 2026

The 2026 Credit Union Digital Branch brings together various data sources for a holistic member view.

Fitts's Law—the time to reach a target is a function of its distance and size—has profound implications for mobile banking design. On a 6.7-inch smartphone display, the "thumb zone" (the arc reachable by the dominant thumb without repositioning the hand) contains roughly 40% of the screen. Every primary action must fall within this zone, or interaction costs skyrocket.

In 2026, 68% of all credit union digital transactions originate from mobile devices, with the remaining 32% split between desktop and tablet. This distribution demands a mobile-first architecture where the desktop experience is an enhancement of the mobile layout, not the other way around. Leading credit unions now design their core interaction patterns for a 375-pixel viewport first, then progressively enhance for larger screens.

The technical implementation involves responsive breakpoints at 375px (small phone), 428px (large phone), 768px (tablet), and 1200px (desktop), with each tier adding capabilities rather than rearranging fundamentals. Touch targets must be a minimum of 48x48 CSS pixels (per WCAG 2.2 requirements) with 8px spacing between adjacent targets to prevent mis-taps. Gesture-based navigation—swipe to transfer, pull to refresh, long-press to favorite—supplements traditional button-based interaction for power users.

The ROI of mobile optimization is measurable: credit unions that achieve mobile performance scores above 90 on Google's Lighthouse report 23% higher mobile conversion rates and 31% longer session durations compared to those scoring below 70.

From Automation to Empathy: Next-Gen AI Integration

The first generation of banking AI—rule-based chatbots that could answer "What are your hours?"—is extinct. The 2026 landscape demands AI systems that understand context, emotion, and intent. When a member searches for "help with payments," the system must distinguish between someone exploring auto-pay options (informational intent) and someone in financial distress (emotional intent requiring empathetic escalation).

Modern credit union AI operates on three tiers: reactive (answering questions), proactive (anticipating needs), and empathetic (detecting emotional states). The empathetic tier uses natural language processing to identify stress markers in member communications—increased typing speed, negative sentiment, urgent language—and automatically routes these interactions to human specialists while adjusting the digital interface to display financial hardship resources prominently.

On the proactive tier, predictive models analyze transaction patterns to surface timely recommendations. A member whose direct deposit increased by 15% might receive a savings optimization suggestion; a member with recurring subscription charges might be shown the credit union's cash-back credit card. These aren't generic cross-sells—they're personalized, contextually relevant interventions that members describe as "helpful" rather than "salesy" in satisfaction surveys.

The technical foundation is a real-time decision engine that processes member signals across channels—mobile app usage, web browsing patterns, call center transcripts, and transaction data—to build a unified behavioral profile. Privacy is paramount: all processing occurs within the credit union's secure environment, and members retain granular control over what data informs AI recommendations.

The "Member 360" View and Hyper-Personalization

The "Member 360" concept aggregates every touchpoint—digital banking sessions, branch visits, call center interactions, loan applications, and community event attendance—into a single, actionable profile. This isn't merely a CRM; it's a living model of the member's financial journey that informs every interaction across every channel.

Hyper-personalization goes beyond segmentation. Rather than grouping members into broad cohorts ("millennials" or "high-net-worth"), the 2026 approach treats each member as a segment of one. The digital branch dynamically adjusts its layout, content, and product recommendations based on the individual's behavior patterns, life stage, and expressed preferences. A first-time homebuyer sees mortgage calculators and homeowner's insurance options prominently; a retiree sees CD rates and estate planning resources.

The implementation requires a Customer Data Platform (CDP) that ingests data from core banking, digital channels, marketing automation, and third-party enrichment sources. Machine learning models trained on historical conversion data identify which product recommendations are most likely to resonate with each member profile, and the content management system dynamically assembles page layouts from modular components based on these predictions.

Early adopters report that hyper-personalized digital branches achieve 2.8x higher product attachment rates than static, one-size-fits-all interfaces. More critically, members who experience personalized interactions show 40% higher retention rates over a three-year period—a direct, measurable impact on the credit union's long-term financial sustainability.

ADA Sovereignty: Accessibility as a Strategic Advantage

In 2026, ADA compliance is no longer a checkbox exercise—it's a strategic differentiator. The DOJ's 2025 ruling explicitly classified financial institution websites as "places of public accommodation" under Title III of the ADA, and the litigation landscape has shifted from warning letters to class-action lawsuits with six-figure settlements. But the real opportunity lies beyond compliance: the 61 million Americans with disabilities represent an underserved market with $490 billion in annual disposable income.

WCAG 2.2 Level AA compliance—the current legal standard—requires keyboard navigability, screen reader compatibility, sufficient color contrast ratios (4.5:1 for body text, 3:1 for large text), visible focus indicators, and consistent navigation patterns. But true accessibility sovereignty goes further: it anticipates needs that formal guidelines don't yet address, such as cognitive accessibility for members with learning disabilities, reduced motion for vestibular disorders, and plain language alternatives for complex financial terminology.

The technical implementation includes ARIA labels on all interactive elements, semantic HTML5 structure, skip navigation links, properly associated form labels, and automated accessibility testing integrated into the CI/CD pipeline. Leading credit unions run monthly audits with both automated tools (axe-core, WAVE) and manual testing with assistive technology users to catch issues that automated scanners miss.

The business case is compelling: accessible websites consistently outperform their inaccessible counterparts on SEO metrics (Google's Core Web Vitals are heavily correlated with accessibility best practices), and credit unions that achieve WCAG 2.2 AA certification report 18% increases in organic search traffic within six months of remediation.

The Psychology of Choice: Engineering Lower Friction, Higher ROI

The Paradox of Choice—Barry Schwartz's seminal research demonstrating that more options lead to fewer decisions—is the silent killer of credit union conversion rates. When a loan page presents 14 product variations with complex eligibility criteria, the cognitive burden drives 67% of visitors to abandon without applying. The 2026 approach limits visible choices to three at any decision point, with clear differentiation and a recommended default.

Loss aversion—the principle that losses are felt 2.3x more intensely than equivalent gains—informs how product benefits are framed. Instead of "Save $200/month with our refinance program," the 2026 copy reads "You're currently paying $200/month more than necessary." The same value proposition, reframed as a loss being incurred, increases click-through rates by 35-40%.

Social proof mechanisms—"4,200 members refinanced this quarter" or "Highest-rated mobile app among regional credit unions"—reduce perceived risk by leveraging the bandwagon effect. Urgency triggers ("Rate lock expires in 48 hours") create temporal scarcity that accelerates decision timelines without resorting to manipulative dark patterns.

The conversion architecture follows a sequential commitment model: each step in the funnel asks for slightly more investment than the previous one, building psychological momentum. The first step (rate check) requires only a zip code. The second (pre-qualification) adds income range. The full application comes third, after the member has already invested enough effort to trigger the sunk cost fallacy. This graduated approach reduces initial friction while maintaining completion rates above 72%.

Reducing "Time-to-Value" (TTV) for New Members

Time-to-Value measures how quickly a new member experiences the core benefit they joined for. If someone opens a checking account expecting mobile deposit capability, TTV is the elapsed time between account approval and their first successful mobile check deposit. In 2026, the benchmark is under 4 minutes—from approval to first productive use.

The onboarding architecture that achieves this speed relies on three principles: parallel processing (identity verification runs concurrently with account provisioning), progressive activation (core features unlock immediately while secondary features configure in the background), and contextual guidance (just-in-time tutorials that surface at the exact moment a member encounters a new feature for the first time).

The first 72 hours after account opening are critically important. Members who complete three or more transactions within this window show 85% retention at the 12-month mark, compared to 41% for those who don't engage within the first week. The digital branch must therefore engineer these early interactions through a carefully orchestrated welcome sequence: an immediate prompt to set up direct deposit (Day 1), a guided bill pay walkthrough (Day 2), and a savings goal introduction (Day 3).

Gamification elements—progress bars showing "account setup completion" at 60%, achievement badges for first mobile deposit, streak counters for consecutive login days—leverage the endowment effect to encourage continued engagement. These elements must be tasteful and aligned with the credit union's brand identity; a community-focused institution might frame achievements as "community milestones" rather than individual "power user" badges.

The Infrastructure of Trust: Security, Speed, and Scalability

The technical infrastructure underlying a 2026 digital branch must satisfy three competing demands simultaneously: security (protecting member data from increasingly sophisticated threats), speed (sub-200ms response times under peak load), and scalability (handling 10x traffic spikes during promotional campaigns or rate announcements without degradation).

The security layer begins with a zero-trust architecture that authenticates every request, encrypts all data in transit (TLS 1.3) and at rest (AES-256), and implements defense-in-depth with Web Application Firewalls (WAF), DDoS protection, and real-time threat intelligence feeds. Content Security Policy headers prevent XSS attacks, Subresource Integrity ensures third-party scripts haven't been tampered with, and HTTP Strict Transport Security eliminates protocol downgrade attacks.

Speed is achieved through a multi-layer caching strategy: CDN edge caching for static assets (99th percentile latency under 50ms), application-level caching for personalized content fragments (Redis with 5-second TTL), and database query optimization with read replicas for report-heavy operations. Core Web Vitals targets—Largest Contentful Paint under 1.5 seconds, First Input Delay under 50ms, Cumulative Layout Shift under 0.05—are enforced through automated CI/CD checks that reject deployments failing these thresholds.

Scalability is addressed through containerized microservices deployed on Kubernetes, with horizontal pod autoscaling triggered by CPU utilization and request queue depth. The architecture supports gradual rollouts (canary deployments) that expose new features to 5% of traffic before full release, enabling real-time performance monitoring and instant rollback if metrics degrade.

Biometric Sovereignty: Beyond the Password

Passwords are dead. In 2026, the most secure credit union digital branches have eliminated traditional passwords entirely in favor of biometric and passkey-based authentication. FIDO2/WebAuthn standards enable device-bound credentials that can't be phished, replayed, or brute-forced, while biometric verification (fingerprint, facial recognition, voice print) provides a seamless second factor.

The concept of "biometric sovereignty" extends beyond authentication to authorization. High-value transactions—wire transfers above $5,000, beneficiary changes, address updates—require step-up biometric verification that occurs inline without redirecting the member to a separate authentication flow. The experience is continuous: the member taps "confirm transfer," a brief facial recognition check occurs, and the transaction completes—all within the same UI context.

Privacy concerns around biometric data are addressed through on-device processing. The biometric template (a mathematical representation of the fingerprint or facial features) never leaves the member's device; the server receives only a cryptographic assertion that the local biometric check passed. This architecture eliminates the risk of centralized biometric database breaches—a critical consideration given the immutable nature of biometric identifiers.

Behavioral biometrics add a passive, continuous authentication layer by analyzing typing patterns, swipe gestures, device orientation, and navigation behaviors to build a behavioral fingerprint. Deviations from the established pattern trigger invisible risk scoring that can require additional verification—all without disrupting the member's workflow unless genuinely anomalous behavior is detected.

Member-Centric Growth: Beyond Transactional Interaction

The 2026 digital branch redefines growth from "acquiring new accounts" to "deepening existing relationships." The metric that matters isn't member count—it's products per member and wallet share. A credit union with 50,000 members averaging 4.2 products each generates more revenue and demonstrates stronger community impact than one with 100,000 members averaging 1.8 products.

The digital branch architecture supports this deepening through lifecycle-triggered engagement campaigns. When a member's savings account crosses the $10,000 threshold, the system automatically surfaces a certificate (CD) comparison calculator. When transaction data indicates a recurring daycare payment, the system offers education savings plan information. When a member's auto loan enters its final 12 months, the system proactively presents refinance options for their next vehicle purchase.

Cross-sell effectiveness depends on timing and relevance. The recommendation engine uses a "next best action" model that evaluates dozens of potential offers against the member's current state and selects the one with the highest predicted relevance score. Offers that a member has previously dismissed are suppressed for a configurable cooling-off period, preventing the "subscription box" fatigue that plagues less sophisticated systems.

The data shows that digitally-engaged members who receive personalized product recommendations maintain an average relationship value 2.4x higher than those who don't. Equally important, these members are 3x more likely to refer friends and family—creating an organic acquisition flywheel powered by member satisfaction rather than marketing spend.

Gamification and Financial Health Mastery

Gamification in credit union digital branches has matured beyond gimmicky point systems. The 2026 approach draws on Self-Determination Theory—the framework that intrinsic motivation is driven by autonomy, competence, and relatedness—to create financial wellness programs that members genuinely value.

Financial health "challenges"—such as a 30-day spending reduction challenge or a 90-day emergency fund builder—provide structure and accountability. Progress visualization (thermometer-style progress bars, milestone celebrations with confetti animations, streak counters) leverages the Zeigarnik Effect, where incomplete tasks create psychological tension that motivates completion. Members who participate in gamified savings challenges save 47% more than those using traditional savings accounts.

Leaderboards, when implemented carefully, tap into the relatedness dimension. Anonymous community leaderboards ("You saved more than 72% of members this month") provide social comparison without privacy concerns. Collaborative goals—"Together, our members have saved $2.3M this quarter toward emergency funds"—reinforce the credit union's cooperative identity and create a sense of shared purpose.

The technical implementation uses event-driven architecture to track member actions in real time and trigger gamification responses instantly. A deposit into a savings goal account triggers an immediate progress bar animation and, upon reaching a milestone (25%, 50%, 75%, 100%), generates a push notification with a celebratory message and the option to share the achievement (anonymized) with the community. These micro-interactions maintain engagement between major financial events.

Community Impact Visualization for the Digital Age

Credit unions exist to serve their communities, and the 2026 digital branch makes this mission tangible through impact visualization. Rather than abstractly claiming "people helping people," leading institutions now display real-time community impact dashboards that quantify the credit union's local footprint: total local loans funded, small businesses supported, financial literacy workshops conducted, and charitable contributions made.

Interactive maps show where the credit union's lending activity concentrates, overlaid with community development metrics like job creation and homeownership rates. Member contributions to shared goals—"Our members collectively saved $14.2 million this year"—reinforce the cooperative advantage and differentiate the credit union from profit-driven competitors.

Individual members see their personal impact within this larger context: "Your deposits this year helped fund 3 local small business loans." This connection between personal financial activity and community benefit creates an emotional bond that transcends the transactional relationship, which is the key differentiator credit unions hold over banks and fintechs.

The implementation leverages data from the core banking system to calculate impact metrics in real time. A feed of recently funded loans (with borrower permission) creates a human storytelling element: "Maria in Springfield used her credit union auto loan to purchase a reliable car for her 45-minute commute." These stories, rotated dynamically on the digital branch homepage, embody the credit union mission in a way that marketing copy never could.

SEO Dominance and Search Generative Optimization (SGO)

Search engine optimization for credit unions in 2026 operates on two fronts: traditional SEO (optimizing for Google's crawl-and-rank algorithm) and the emerging discipline of Search Generative Optimization (SGO)—ensuring the credit union's content is selected as a source by AI-generated search summaries.

Traditional SEO fundamentals remain critical. Technical SEO demands clean URL structures, proper canonical tags, XML sitemaps, schema.org structured data (LocalBusiness, FinancialProduct, FAQPage, BreadcrumbList), and Core Web Vitals scores in the "Good" range. Content SEO requires topical authority—comprehensive coverage of credit union-relevant subjects like mortgage education, financial wellness, and community development—supported by strategic internal linking and authoritative external citations.

SGO adds a new dimension: AI search engines (Google's AI Overviews, Perplexity, etc.) synthesize answers from multiple sources, and the content most likely to be cited is that which provides clear, factual, and well-structured information with specific data points. Credit unions that publish long-form, data-rich articles with proper heading hierarchy, FAQ schema, and cited statistics see 3-5x more AI citation mentions than those with thin, generic content.

Local SEO—optimizing for "credit union near me" and branch-specific queries—remains a high-ROI channel. A fully optimized Google Business Profile, consistent NAP (Name, Address, Phone) data across directories, localized landing pages for each branch, and an active review management strategy (responding to 100% of Google reviews within 24 hours) compound to drive 40-60% of new member acquisition for community-focused institutions.

Content-as-a-Service: Building Authority and Trust

The 2026 digital branch positions the credit union as a trusted financial educator, not merely a service provider. A comprehensive content strategy—publishing 2-4 in-depth articles per week on topics ranging from first-time homebuyer guides to retirement planning calculators—builds the topical authority that drives both SEO performance and member trust.

Content is structured as a service layer that integrates with the digital banking experience. When a member views their mortgage details, a contextual sidebar suggests relevant articles: "5 Ways to Build Equity Faster" or "Understanding Your Escrow Account." When a member's transaction history shows restaurant spending above their budget threshold, a notification links to a meal planning on a budget guide. Content isn't siloed on a blog—it's woven into the financial experience at every relevant touchpoint.

The content architecture follows the hub-and-spoke model: comprehensive "hub" pages cover broad topics (e.g., "The Complete Guide to Credit Union Mortgages"), while detailed "spoke" articles address specific subtopics (e.g., "FHA vs. Conventional Loans for First-Time Buyers"). Internal links between hubs and spokes create a semantic web that search engines interpret as deep topical expertise, boosting domain authority and page-level rankings.

Video content—short-form explainers (under 90 seconds), member testimonial stories, and virtual branch tours—complements written content and performs particularly well in social media distribution. Credit unions that maintain an active YouTube presence report 28% higher brand awareness scores and 15% faster member acquisition rates compared to those relying solely on written content.

Case Studies and Actionable ROI Metrics

The business case for digital branch transformation is supported by consistent, measurable outcomes across early-adopting credit unions. A $400M community credit union in the Midwest invested $180,000 in a comprehensive digital branch redesign and tracked the following metrics over 12 months:

- Mobile banking adoption increased from 34% to 71% of active members

- Loan application completion rates improved from 28% to 64% (+129%)

- Average products per member rose from 2.1 to 3.4

- Net Promoter Score improved from 42 to 68

- Call center volume decreased by 31%, reducing operational costs by $220,000 annually

- New member acquisition increased 22% year-over-year, with 48% citing "digital experience" as a primary selection factor

The payback period for the investment was 9.8 months, with an ongoing annual ROI of 183%. These metrics are consistent with industry benchmarks reported by Filene Research Institute and CUNA.

A second case study—a $1.2B credit union serving a major metropolitan area—focused specifically on mobile optimization and AI integration. Their results included a 45% reduction in mobile session abandonment, a 38% increase in digital loan originations, and a 52% improvement in member satisfaction scores for the under-35 demographic. The credit union attributes $3.4M in incremental loan revenue directly to the digital transformation initiative.

The 2026 Implementation Roadmap: Phased Transformation

Transforming a legacy digital presence into a 2026-ready digital branch is a 12-18 month initiative best executed in four phases:

Phase 1: Foundation (Months 1-3) — Technical infrastructure audit, Core Web Vitals remediation, accessibility assessment, and hosting/CDN optimization. Deliverables: sub-3s load time, WCAG 2.1 AA compliance, and a mobile Lighthouse score above 80. Budget allocation: 20% of total investment.

Phase 2: Experience (Months 4-8) — UX redesign based on member research, dashboard velocity optimization, mobile-first responsive architecture, and onboarding flow re-engineering. Deliverables: new member portal, redesigned loan application funnel, and TTV reduction to under 5 minutes. Budget allocation: 40% of total investment.

Phase 3: Intelligence (Months 9-12) — AI integration, personalization engine deployment, predictive product recommendation system, and behavioral analytics implementation. Deliverables: Member 360 profile, automated cross-sell campaigns, and proactive financial wellness alerts. Budget allocation: 25% of total investment.

Phase 4: Optimization (Months 13-18) — Continuous A/B testing, conversion rate optimization, content strategy execution, SEO/SGO buildout, and advanced gamification deployment. Deliverables: measurable KPI improvements across all tracked metrics, with monthly optimization sprints. Budget allocation: 15% of total investment.

Each phase builds on the previous one, and intermediate milestones allow the credit union to demonstrate ROI incrementally—securing continued executive support for the long-term transformation.

Conclusion: The Future of the Digital Branch

The 2026 credit union digital branch is not a website with a login page bolted on. It's a living, intelligent ecosystem that anticipates member needs, delivers sub-second interactions, and continuously adapts based on behavioral data. It combines the warmth and community orientation that defines the credit union movement with the technical sophistication of the world's best fintech platforms.

The institutions that thrive in 2026 and beyond will be those that recognize their digital branch as their primary branch—the first touchpoint for 78% of member interactions and the engine that powers relationship deepening, community impact, and sustainable growth. The technology exists. The frameworks are proven. The ROI is documented. The only remaining variable is the decision to act.

For credit unions ready to architect their high-velocity digital future, the time to begin is now. Every quarter of delay is a quarter of member attrition, competitive displacement, and unrealized revenue.

Frequently Asked Questions

Q: How much does a full digital branch transformation cost for a mid-size credit union?

A: Budget expectations range from $120,000 to $350,000 for credit unions between $200M and $1B in assets, depending on the scope of AI integration and custom development required. Most institutions see full ROI payback within 10-14 months.

Q: Can we implement the digital branch in stages, or does it require a complete overhaul?

A: A phased approach is strongly recommended. The 4-phase implementation roadmap outlined above allows credit unions to realize incremental value at each stage while managing risk and budget constraints.

Q: What are the minimum technical requirements for WCAG 2.2 AA compliance?

A: Key requirements include keyboard navigability for all functions, screen reader compatibility, 4.5:1 color contrast for body text (3:1 for large text), visible focus indicators, consistent navigation, error identification and suggestion, and minimum 24x24 CSS pixel touch targets (48x48 recommended). Automated tools catch approximately 30-40% of issues; manual testing with assistive technology is essential.

Q: How do we measure the ROI of AI personalization in digital banking?

A: Track product attachment rates (products per member), recommendation click-through rates, conversion rates on personalized vs. non-personalized offers, member retention rates by engagement level, and Net Promoter Score trends. A/B testing personalized vs. static experiences provides the clearest causal evidence.

Q: What timeline should we expect for measurable SEO improvements after a digital branch redesign?

A: Technical SEO improvements (Core Web Vitals, site speed) typically produce ranking gains within 4-8 weeks. Content authority building through topical hub-and-spoke strategies shows measurable organic traffic growth within 3-6 months. Local SEO optimizations can produce results within 2-4 weeks for map pack visibility.