📑 Table of Contents

- Why Video Banking Matters More Than Ever in 2026

- The Core Use Cases Driving Video Banking Adoption

- Technology Infrastructure: What You Actually Need to Build

- Designing the Member Video Experience: It Is Not Just a Phone Call on Camera

- Staffing Models: Who Takes the Call and How Training Changes

- Compliance, Security, and Privacy in Video Banking

- Building Your Video Banking Roadmap: A Phased Approach

- Integration with Core Systems and Member Data

- Measuring ROI: Beyond Cost Savings to Member Loyalty

- Marketing Your Video Banking Service to Members

- The Future of Video Banking: AI-Augmented, Predictive, and Always On

- References

- 📑 Table of Contents

Table of Contents

For decades, walking into a credit union branch meant one thing: looking a friendly teller in the eye, shaking a loan officer’s hand, and feeling the human connection that community financial institutions have always prided themselves on. That experience built trust. It built loyalty. It built the credit union movement itself. But in 2026, that handshake is increasingly happening through a screen – and that is not a compromise. It is an evolution.

Video banking has emerged as one of the most major tools in the credit union technology stack. Unlike chatbots, text-based support, or phone calls, video banking preserves the human element of credit union service while meeting members where they increasingly live – online, on mobile, and on their own schedules. Credit unions that implement video banking strategically are not just keeping up with megabanks; they are differentiating themselves by doubling down on the relationships that have always set them apart.

This article explores the full space of video banking for credit unions in 2026. We will cover the technology infrastructure required, the member experience design principles that make or break video interactions, staffing and training considerations, compliance and security requirements, and how to measure ROI on your video banking investment. Whether you are evaluating your first video banking solution or looking to optimize an existing deployment, this guide provides the strategic framework you need.

📑 Table of Contents

Why Video Banking Matters More Than Ever in 2026

The numbers tell a clear story. According to recent industry surveys, more than 60 percent of credit union members now prefer digital-first interactions for routine transactions, yet a majority still say they value face-to-face relationships when making important financial decisions like loan applications, financial planning, or resolving complex service issues. Video banking bridges that gap with remarkable efficiency.

Credit unions face a unique challenge in the 2026 space. Megabanks like Chase and Bank of America have enormous technology budgets and can deploy sophisticated digital tools at scale. FinTechs like Chime and SoFi offer slick, mobile-first experiences with no branches at all. Credit unions cannot win on technology budget alone, and they should not try to. What they can win on is trust, personalization, and genuine human connection – and video banking is the digital channel that makes those qualities tangible even at a distance.

The pandemic era forced a rapid adoption of video communication across every industry, and banking was no exception. But what started as a stopgap during lockdowns has become a permanent expectation. Members now expect the ability to connect face-to-face with a trusted advisor from their living room, their office, or even their car. Credit unions that invested in video banking early are seeing measurable results: higher member satisfaction scores, faster loan closing times, and reduced branch traffic for routine inquiries that frees up in-person staff for higher-value interactions.

Beyond member preference, there is a strategic imperative. The branch network that served credit unions well for a century is becoming prohibitively expensive to maintain at current levels. Real estate costs, staffing shortages, and changing consumer behavior are forcing difficult decisions about branch footprints. Video banking offers a viable path forward: maintain the intimacy of branch service without the overhead of physical locations. It is not about replacing branches entirely, but about extending their reach.

The Core Use Cases Driving Video Banking Adoption

Video banking is not a single service. It is a platform that supports multiple distinct use cases, each with different requirements for technology, staffing, and member experience design. Understanding this space is the first step in building a strategy that delivers real value rather than just checking a technology box.

The most common and highest-volume use case is video teller services. A member connects with a teller via video to conduct routine transactions – deposits, withdrawals, check cashing, balance inquiries – that would traditionally require a visit to a branch. These sessions are typically brief, structured, and highly transactional. The technology requirements are straightforward: reliable two-way video, secure document handling, and integration with the core processing system to execute transactions in real time.

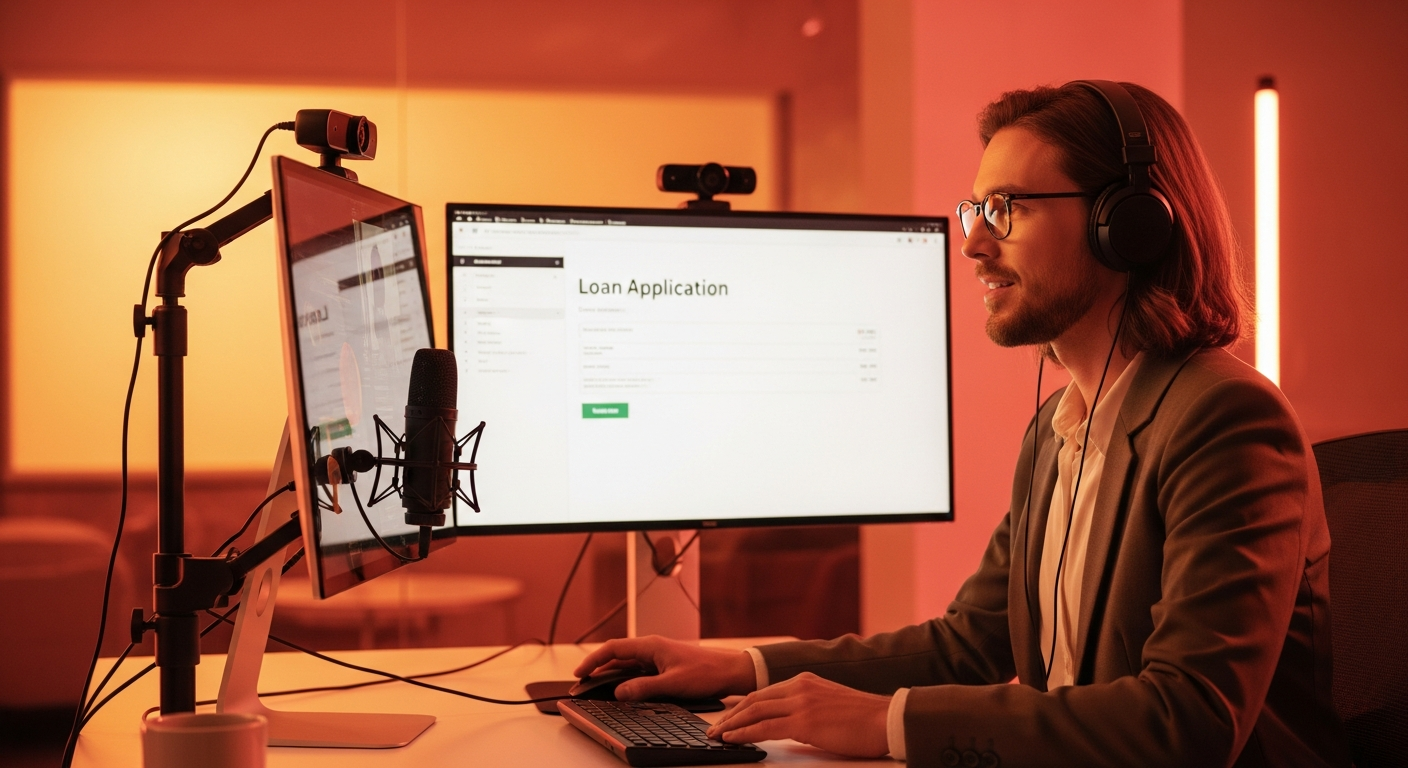

Loan origination via video has emerged as one of the highest-value use cases. A member applies for a mortgage, auto loan, or personal line of credit and completes the process with a live loan officer via video. This is not a phone call with a shared screen. It is a fully interactive session where the loan officer can guide the member through document uploads, e-signatures, credit disclosures, and real-time decisioning. Credit unions using video for loan origination report closing rates 20 to 30 percent higher than phone-based or fully automated digital applications, precisely because the human element builds confidence and trust during a high-stakes financial decision.

Financial counseling and advisory services represent a third major use case. Members schedule video appointments with financial advisors for retirement planning, college savings strategies, debt management, or major purchase planning. These sessions are longer, more consultative, and require a richer set of collaboration tools – shared whiteboards, document co-browsing, screen sharing, and interactive calculators. For credit unions positioning themselves as trusted financial partners rather than transaction processors, this use case is arguably the most strategically important.

Dispute resolution and fraud reporting, while lower in volume, are high in value. When a member discovers a fraudulent charge or needs to dispute a transaction, the emotional stakes are high. A video interaction allows the credit union to demonstrate urgency, empathy, and competence in ways that a phone call or email cannot match. Members who resolve sensitive issues via video report significantly higher satisfaction and are more likely to recommend the credit union to others.

Finally, video banking serves a critical accessibility function. Members with disabilities, members in rural areas with limited branch access, and members with mobility challenges all benefit from the ability to access face-to-face service remotely. This is not merely a convenience issue – it is an equity issue, and credit unions that treat video banking as an accessibility tool demonstrate genuine commitment to inclusive service.

Technology Infrastructure: What You Actually Need to Build

Implementing video banking requires more than just buying a webcam and opening a Zoom account. The technology infrastructure must support security, compliance, integration, and scale. Understanding the components of a robust video banking platform will help you evaluate vendors and make informed infrastructure decisions.

The foundation is your video communication platform. This is the engine that handles real-time audio and video streaming, and it must meet banking-grade requirements for reliability, latency, and encryption. WebRTC (Web Real-Time Communication) has become the industry standard, enabling peer-to-peer video through web browsers and mobile apps without requiring members to download additional software. Leading video banking platforms build on top of WebRTC, adding features like session recording, queue management, and screen sharing.

Session recording and storage is a regulatory requirement, not a nice-to-have. Every video interaction must be securely recorded, timestamped, and stored in compliance with record retention policies. The storage infrastructure must support encryption at rest, access controls, and automated purging based on retention schedules. Cloud-based storage with geo-redundancy is the standard approach, but credit unions must verify that their provider meets NCUA and state-level data residency requirements.

Document handling capabilities are critical and often overlooked. Members need to be able to upload identification documents, signed forms, financial statements, and other paperwork during a video session. The platform must support secure document transmission, optical character recognition for data extraction, and seamless transfer of documents to the core system or document management platform. Integration with e-signature providers like DocuSign or Adobe Sign is essential for loan origination workflows.

Queue management and routing technology determines how efficiently members connect with the right staff member. A sophisticated video banking platform will offer intelligent routing based on the purpose of the call, member segment, language preference, and staff availability. Members should not have to repeat their story every time they are transferred. The system should maintain context across interactions and route to the appropriate specialist on the first attempt.

Integration middleware connects the video platform to your core processing system, CRM, loan origination system, and other backend platforms. This is where many video banking implementations fail. Without deep integration, staff must manually enter data from video interactions into multiple systems, defeating the efficiency gains that video banking promises. API-first platforms that offer pre-built connectors for popular core systems like Symitar, Episys, and Cuiserv are worth the premium over generic video conferencing tools.

Bandwidth and network infrastructure at the branch and staff level is another frequently underestimated requirement. High-quality video requires consistent upload and download speeds of at least 10 Mbps per session. Credit unions deploying multiple simultaneous video sessions across a branch must ensure their network infrastructure can handle the load without degrading quality. A choppy, pixelated video experience damages member trust and undermines the entire investment.

Designing the Member Video Experience: It Is Not Just a Phone Call on Camera

The single biggest mistake credit unions make with video banking is treating it as a phone call with a camera turned on. The member experience for video interactions is fundamentally different from phone or in-person service, and it requires intentional design to get right. A poorly designed video experience will drive members back to branches or, worse, to competitors.

First impressions matter enormously in video banking. The moment a member initiates a video session, they should feel welcomed and guided. The interface should clearly communicate what to expect: how long the wait will be, what information to have ready, and how the session will proceed. A loading screen with a generic spinner is not acceptable. Progressive disclosure – showing members step-by-step what is happening – reduces anxiety and builds confidence in the digital channel.

Camera positioning and eye contact are subtle but critical design elements. Research consistently shows that members trust representatives more when they appear to be making eye contact, which means the camera should be positioned as close to eye level as possible. Staff training should cover proper camera positioning, lighting, and background considerations. Credit unions should provide staff with professional-grade webcams and lighting kits rather than relying on built-in laptop cameras that produce unflattering, low-quality video.

Screen layout and information architecture during a video session require careful thought. What does the member see on their screen during the call? The video feed of the representative should be prominent but not dominant. Members also need access to transaction details, document upload interfaces, chat for sharing links or information, and status indicators for processes happening in the background. The interface should not feel cluttered or overwhelming. A clean, focused layout with clear calls to action for the next step in the process is essential.

Audio quality is arguably more important than video quality. Members will forgive an occasionally pixelated video far more readily than they will forgive echo, background noise, or dropped audio. Invest in high-quality microphones and noise cancellation technology. Train staff to use headsets rather than speakerphone-style setups. Test audio quality from various device types – desktop, laptop, tablet, phone – to ensure a consistent experience across member hardware.

The end of a video session deis much design attention as the beginning. Members should leave the interaction with clear next steps, a confirmation or receipt, and an easy way to schedule a follow-up if needed. The session should not end abruptly when the representative hangs up. A graceful exit flow that confirms the session is complete, summarizes what was accomplished, and offers feedback collection sets the stage for future video interactions.

Staffing Models: Who Takes the Call and How Training Changes

Video banking demands a different approach to staffing than traditional branch or call center models. The person on camera is not just performing a transaction; they are representing the credit union’s brand, building trust, and managing a complex interaction that blends technical skills with interpersonal connection. Not every employee is suited for video banking, and the ones who are need different training than their branch-based counterparts.

Centralized video banking teams have become the dominant staffing model among credit unions with successful deployments. Rather than routing video calls to individual branch tellers, these credit unions establish dedicated video banking teams housed in a central location or distributed across a small number of video hubs. Centralization enables consistent service quality, better coverage across business hours, more efficient staffing, and deeper specialization among team members.

The skills required for video banking are distinct. Staff need strong verbal communication since they cannot rely on the physical cues of an in-person interaction. They need technical comfort with the video platform, document handling tools, and core system interfaces, all while maintaining a natural conversation. They need emotional intelligence to read member sentiment through a camera and adjust their approach accordingly. And they need the discipline to maintain professional appearance, lighting, and camera presence for the duration of every shift.

Training for video banking should cover four core areas. Technical training ensures staff can handle the platform, troubleshoot common issues, and handle document workflows without fumbling. Communication training focuses on active listening, clear articulation, and the specific verbal techniques that build trust through video. Appearance and environment training covers dress code, background selection, lighting setup, and camera positioning. Simulation training, where staff practice video sessions with peers before taking live calls, is essential for building confidence and identifying improvement areas.

Performance metrics for video banking staff differ from traditional call center metrics. Average handle time is less important than first-contact resolution and member satisfaction. Quality assurance scoring should evaluate factors specific to video: camera presence, audio clarity, screen sharing effectiveness, and the smoothness of transitions between tasks during the session. Leading credit unions use post-session surveys and video review to provide coaching feedback to staff.

Scheduling and capacity planning for video banking requires a data-driven approach. Analyze historical call volumes by time of day, day of week, and season to determine staffing requirements. Build in buffer capacity for unexpected surges. Consider extended hours for video banking – many members prefer video interactions during evenings and weekends when branches are closed. Flexible staffing models that include part-time and remote workers can help cover extended hours without excessive overtime costs.

Compliance, Security, and Privacy in Video Banking

Video banking introduces compliance and security considerations that go beyond traditional branch or phone-based interactions. Credit unions must handle a complex regulatory space that includes NCUA requirements, state privacy laws, the Gramm-Leach-Bliley Act, and increasingly stringent data protection standards. Getting compliance right is not optional, and getting it wrong carries serious consequences.

Identity verification is the first and most critical security requirement. When a member appears on video, how do you know they are who they say they are? The answer requires a layered approach. Knowledge-based authentication (KBA) questions remain a baseline, but they are increasingly vulnerable to data breaches and social engineering. Video banking platforms should support multi-factor authentication, including one-time passcodes sent to the member’s registered device, biometric verification, and government ID scanning during the session.

Session recording and retention must comply with applicable recordkeeping regulations. Credit unions must record all video banking sessions and retain them according to their document retention schedule, typically five to seven years depending on the transaction type. Recordings must be stored securely with encryption at rest, and access must be logged and audited. Members should be notified that sessions are being recorded, and the notification should be captured in the recording itself to demonstrate compliance.

Data privacy during video sessions requires careful attention. Staff should not have visible personal information in their background – no whiteboards with member details, no visible computer screens showing other member accounts. Screen sharing must be tightly controlled to prevent accidental exposure of sensitive data. The video platform itself must use end-to-end encryption for all audio and video streams, and the provider must sign a business associate agreement or equivalent data processing agreement.

State-level privacy laws add complexity for credit unions operating across multiple states. The California Consumer Privacy Act (CCPA), Virginia’s Consumer Data Protection Act (VCDPA), and similar laws in other states impose requirements around data collection, storage, and member rights that apply to video banking recordings and metadata. Credit unions must know which states their members reside in and ensure their video banking processes comply with each applicable law.

BIPA concerns are particularly relevant for video banking. The Illinois Biometric Information Privacy Act and similar laws in Texas, Washington, and New York regulate the collection and storage of biometric data, including facial geometry captured during video recordings. Credit unions offering video banking to members in these states must implement BIPA-compliant notice, consent, and retention practices. This is a rapidly evolving area of law, and legal counsel should review video banking privacy practices regularly.

Third-party vendor risk management is another critical compliance area. Most credit unions will partner with a video banking platform provider rather than building their own solution. The due diligence process must include security audits, SOC 2 Type II reports, penetration testing results, and a thorough review of the vendor’s data handling practices. The vendor relationship should be governed by a contract that clearly defines data ownership, breach notification procedures, and liability in the event of a security incident.

Building Your Video Banking Roadmap: A Phased Approach

Implementing video banking is a multi-year path, not a single project. Credit unions that try to deploy everything at once typically struggle with change management, technology integration, and adoption. A phased approach that builds momentum and demonstrates value at each stage is more likely to succeed.

Phase one should focus on a single high-value use case with a limited pilot group. Loan origination is an excellent starting point because it delivers clear ROI, involves a manageable volume of interactions, and gives you the opportunity to refine processes before scaling. Select two to three branches or lending teams to participate in the pilot. Define success metrics before launch: loan closing rates, member satisfaction scores, average time to close, and staff confidence ratings.

The pilot should run for 60 to 90 days with intensive monitoring and iteration. Collect feedback from members and staff weekly. Identify pain points in the technology, the workflow, and the member experience. Make adjustments rapidly. Do not be afraid to change course if something is not working. The goal of the pilot is learning, not proving that your initial assumptions were correct.

Phase two expands to additional use cases and a broader member base. Add video teller services for routine transactions, beginning with a small set of branches and gradually expanding. Integrate video banking into the mobile app so members can initiate video sessions directly from their phone. Begin offering video financial counseling for members who request advisory services. This phase typically runs six to twelve months and requires additional staff training and technology investment.

Phase three achieves enterprise-wide deployment with full integration across channels. Video banking is now available for every use case, accessible from every channel (mobile, web, branch kiosks), and staffed by a dedicated team with specialized training. Integration with the CRM means staff see a complete member history when a video session begins. Analytics dashboards provide real-time visibility into queue status, session quality, and member satisfaction. This is the mature state that most credit unions should target within 18 to 24 months of beginning their video banking path.

Throughout all phases, change management is essential. Staff who have spent years building relationships in person may feel threatened or uncertain about video banking. Clear communication about how video banking enhances rather than replaces their role, combined with hands-on training and visible leadership support, will ease the transition. Celebrate early wins and share success stories across the organization to build momentum and enthusiasm.

Integration with Core Systems and Member Data

The quality of your video banking experience is directly proportional to the depth of your integration with core systems. A video banking platform that exists in isolation, requiring staff to toggle between multiple applications and manually enter data, will frustrate both staff and members. Deep integration transforms video banking from a standalone channel into a seamless extension of your member service ecosystem.

CRM integration is the highest priority. When a member initiates a video session, the platform should immediately identify them and surface their complete profile – account relationships, recent interactions, pending applications, service history, and any flagged issues. The staff member answering the call should never have to ask, “Can I have your account number?” or “What can I help you with today?” The context should be delivered automatically.

Core processing integration enables real-time transactions during video sessions. A member who wants to transfer funds, check a balance, make a payment, or update account information should be able to do so without the staff member leaving the video interface. The video platform should write transactions directly to the core system and confirm completion within the video session. This level of integration requires close collaboration with your core provider and may involve custom API development.

Loan origination system integration is essential for video loan applications. The video platform should be able to initiate a loan application, pull credit reports, verify income documents, present disclosures for e-signature, and submit the application for underwriting – all within the video session. Members should not have to fill out paper forms or visit a separate portal. A seamless loan origination experience through video is one of the strongest arguments for investing in deep integration.

Document management integration ensures that all documents collected during video sessions are automatically filed in the correct locations with proper metadata. Receipts, signed forms, identification scans, and disclosure acknowledgments should flow directly from the video session into your document management system without manual intervention. This also creates a complete, auditable record of every video interaction.

Analytics and reporting integration allows you to measure the impact of video banking on business outcomes. Connect your video platform to your business intelligence tools to track metrics like video session volume, average handle time by use case, conversion rates for video-originated loans, and member retention rates among video banking users. These insights justify continued investment and guide ongoing optimization.

Measuring ROI: Beyond Cost Savings to Member Loyalty

Calculating the return on investment for video banking requires looking beyond simple cost comparisons. While video banking does reduce branch traffic and associated costs, the real value comes from revenue growth and member retention. Credit unions that measure ROI narrowly on cost savings alone often undervalue their video banking investment and underinvest in its potential.

The most straightforward ROI calculation is transaction cost reduction. Video teller transactions typically cost 60 to 80 percent less than in-branch teller transactions when accounting for staff time, facility costs, and overhead. If a credit union shifts 20 percent of its branch transactions to video banking, the savings in branch staffing and real estate can be substantial. These savings alone often justify the initial technology investment within 12 to 18 months.

Loan conversion rates tell a more strategic ROI story. Credit unions using video for loan origination report closing rates 20 to 30 percent higher than digital-only applications and 15 to 20 percent higher than phone applications. For a credit union originating 500 loans per month with an average loan value of 25,000 dollars, a 20 percent improvement in conversion rate translates to significant revenue growth. These numbers compound over time as members who originate loans via video become more engaged and loyal.

Member retention is where video banking delivers its most deep but hardest-to-measure returns. Members who use video banking services are measurably more loyal than those who do not. They have a richer relationship with the credit union, they trust the brand more deeply, and they are less likely to shop around for banking services from competitors. A five percent improvement in member retention can increase profitability by 25 to 95 percent according to industry research, making retention improvements from video banking potentially the largest source of long-term value.

Cross-sell and upsell rates increase measurably for video banking users. When a member connects with a trusted advisor via video for one purpose – say, a car loan application – the advisor has a natural opportunity to discuss related needs: gap insurance, credit life insurance, a credit card with a higher limit, or a home equity line of credit. The context-full, personal nature of video interactions creates natural cross-sell opportunities that do not exist in text-based or phone-based service channels.

Net Promoter Score (NPS) improvements are another important ROI metric. Credit unions that deploy video banking consistently see NPS increases of 10 to 20 points for members who use the video channel compared to those who do not. Since NPS correlates strongly with member lifetime value and organic growth through referrals, this improvement has real financial implications. A credit union that grows primarily through member referrals will see a direct impact on acquisition cost as NPS rises.

Staff satisfaction and retention is an often-overlooked ROI factor. Employees who work in video banking roles report higher job satisfaction than those in traditional call center positions, and turnover rates are significantly lower. Reducing call center turnover by even five percent saves meaningful money in recruitment, training, and productivity ramp-up costs. Happy staff also deliver better member experiences, creating a virtuous cycle that reinforces the business case.

Marketing Your Video Banking Service to Members

Building a great video banking experience means nothing if members do not know it exists or do not trust it enough to use it. Marketing video banking requires a deliberate strategy that addresses member awareness, education, and trust barriers. Credit unions that simply add a video banking button to their app and expect adoption are almost always disappointed.

Internal marketing to staff comes first. Before members can adopt video banking, front-line staff must understand it, believe in it, and actively promote it. Every branch employee, call center representative, and loan officer should be able to describe what video banking is, how it benefits members, and how to initiate a video session. Staff who are enthusiastic about video banking become your most effective marketing channel.

Launch campaigns should emphasize convenience and human connection simultaneously. The messaging should position video banking as “branch-quality service from wherever you are” rather than “yet another digital channel.” Use member testimonials in your marketing materials – real members explaining how video banking saved them a trip to the branch or helped them close a loan faster from their kitchen table. Social proof is powerful for overcoming the initial hesitation members might feel about banking via video.

In-app and on-website promotion should make video banking visible at every member touchpoint. When a member is on the loan application page, they should see an option to “Speak with a loan officer via video.” When a member checks their balance on the mobile app, a gentle prompt should offer “Need help? Video chat with us.” When a member calls the contact center, the IVR should offer video banking as a routing option. Contextual promotion drives adoption much more effectively than generic announcements.

Trial and onboarding are critical for converting curious members into regular users. The first video banking experience should be guided and low-pressure. Consider offering a concierge service where a dedicated team member walks the member through their first video session, showing them how it works and answering questions. Members who have a positive first video experience are highly likely to use the service again. Members who struggle or feel confused may never return.

Ongoing engagement should celebrate video banking as a signature credit union service. Feature video banking in your newsletter, on social media, and in branch signage. Share stories of members who have exceptional experiences. Run targeted campaigns to specific member segments – young members, busy professionals, snowbirds, members with disabilities – who are most likely to benefit from and appreciate video banking. Treat video banking not as a utility but as a competitive differentiator worth talking about consistently.

The Future of Video Banking: AI-Augmented, Predictive, and Always On

Video banking in 2026 is impressive, but the technology continues to evolve rapidly. Credit unions making video banking investments today should understand where the technology is heading so they can build a platform that will remain relevant and competitive for years to come. The next wave of video banking innovation will be driven by artificial intelligence, predictive analytics, and ambient computing.

AI-augmented video sessions are already emerging. During a live video interaction, AI can provide real-time assistance to the staff member: surfacing relevant product recommendations based on the member’s transaction history, suggesting talking points based on the member’s recent life events, or automatically populating forms with data extracted from documents the member uploads. The staff member remains in control, but AI handles the background work that currently slows down video interactions and creates friction.

Real-time language translation will make video banking accessible to members who prefer to conduct their financial business in a language other than English. Natural language processing and speech-to-text translation have improved dramatically, and video banking platforms will increasingly offer real-time translation that allows a Spanish-speaking member and an English-speaking representative to have a natural conversation, each hearing the other in their preferred language. This capability is major for credit unions serving diverse communities.

Predictive video banking will move beyond reactive, member-initiated sessions. When predictive analytics detects that a member is likely to need assistance – perhaps they have been spending more than usual, they are approaching a credit limit, or they have experienced a life event like a move or job change – the credit union can proactively offer a video consultation. These proactive outreach sessions build deeper relationships and prevent problems before they escalate.

Video banking kiosks in branch lobbies and remote locations will bridge the gap between digital and physical service. A member walks into a small satellite location or a kiosk in a grocery store, sits down in a private booth, and connects via video to a centralized team of specialists. The kiosk can include document scanners, card printers, and cash dispensers, enabling a full-service banking experience without a full branch staff. This model dramatically reduces the cost of physical presence while maintaining service quality.

Ambient video banking, enabled by always-on devices like smart displays and voice assistants, will make video interactions as simple as saying “I want to talk to someone.” Members will not need to handle an app or find a button. They will simply express their need, and the system will connect them with the right person at the right time. Reducing friction to this level will drive adoption among less tech-savvy members and make video banking the default service channel rather than a specialty option.

The credit unions that will thrive in this future are the ones that start building their video banking foundation today. The technology is mature. The business case is proven. The member demand is clear. The only question that remains is whether your credit union will lead in video banking or follow. Every month of delay is a month of missed opportunity to deepen member relationships, reduce costs, and build the digital trust that will define credit union success for the next decade.

References

- America’s Credit Unions: Digital Banking Research – Industry research on credit union member preferences for digital and remote banking services

- NCUA Regulatory Guidance on Digital Services – Official NCUA guidance on technology service provider oversight and digital banking compliance requirements

- The Financial Brand: Digital Banking Trends – Industry publication covering credit union and banking digital transformation trends and case studies

- Javelin Strategy & Research: Digital Banking – Research reports on digital banking adoption patterns and member behavior across financial institutions

- Illinois BIPA Statute – The Illinois Biometric Information Privacy Act text governing biometric data collection

- Credit Union Times: Technology Coverage – Credit union industry publication covering technology adoption trends and implementation best practices

- American Bankers Association: Digital Banking Resources – Banking industry resources on digital channel strategy, security, and member experience design

- Deloitte: Financial Services Technology Trends – Consulting industry analysis on emerging technologies in financial services including video banking and AI

- Federal Reserve Publications – Federal Reserve publications and data on consumer finance, digital banking trends, and economic well-being

- CFPB Compliance Resources for Digital Financial Services – Consumer Financial Protection Bureau guidance on compliance requirements for digital banking channels

This article was brought to you by GrafWeb CUSO – Building the future of digital credit unions.